Moral Hazard & Adverse Selection

By Randy Edwards and Liviu Florea

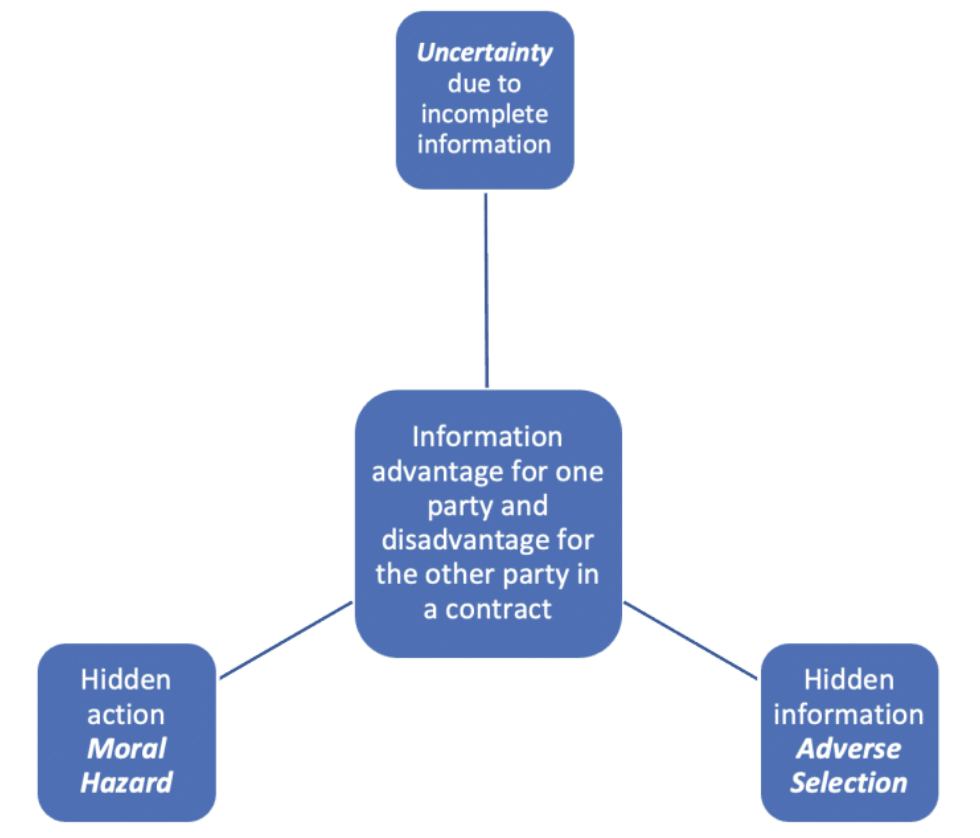

Uncertainty is an inevitable part of our lives. Decision-makers in companies, people at work, customers interacting with service providers, organizations negotiating contracts within their units or with each other, all experience uncertainty. Sometimes uncertainty is symmetric — for example, no one knows next Saturday’s winning lottery numbers.

The more interesting case, however, is that of asymmetric or incomplete information, when one party to a contract has more information than the other. This can breed information disadvantages for one party and advantages for the other party in a contract, making opportunistic behaviors more possible.

Much scholarly work has been done to make sense of these complex scenarios. Arrow (1985) refers to two information advantages: hidden actions, which are actions that cannot be accurately observed or inferred and consequently are not recognized in contracts, and hidden information, which involves developments about which party has incomplete information that may determine that party’s actions but are not fully observable by the other.

In an illustration of hidden action, some employees, seen as one party in the employment contract, who are paid a fixed wage, may have an incentive to misdirect effort and may not use their worktime for the benefit of their employers. To address this possibility, employers may monitor behaviors of their employees at work, spending time, money or other resources, to make sure that their employees really work.

Meanwhile, hidden information can occur during the selection process in organizations where applicants may hide information about themselves that is relevant for the selection decision to increase the likelihood that they will be selected.

Hidden action can lead to moral hazard problems, while hidden information can lead to adverse selection problems. In the employment context, adverse selection exists when parties (e.g., employees or job applicants) misrepresent their true abilities, while moral hazard exists when one party (e.g., managers) does not know with absolute certainty if an employee works hard or hardly works (i.e., avoids work as much as possible).

Principles of agency theory explain how using certain contractual organizational forms helps deter moral hazard and adverse selection.

MORAL HAZARD

Occurs after the transaction or contract is made, in form of behavioral changes. Incentivizes engagement in risky activities.

Moral hazard is defined as the potential for bad-faith action, incomplete, even misleading information, or disingenuous and risky actions for the personal benefit of one party, at the expense of the other party in a contract. When one party has an incentive to take additional risks that a contract or the other party did not anticipate, moral hazard can occur.

If those risks yield benefit, risk-takers may profit; if those risks backfire, losses may be spread out. Moral hazard can also be reflected in suboptimal effort or misdirected effort when risk takers are not kept accountable.

Therefore, moral hazard is manifested in actions intended to maximize one party’s utility to the detriment of the other party. These actions can occur when agents do not bear the full consequences of their actions.

Initially developed in the insurance industry, the concept of moral hazard addresses potential situations wherein an insurance policy allows or induces undesirable behaviors. This concept was extended to other areas of inquiry, including corporate control, where moral hazard can occur when managers, acting as agents for shareholders, behave in ways that reduce shareholder value (i.e., act against principals’ interest).

One manifestation of moral hazard was offered by Arrow (1971), who likened equity ownership to a managerial insurance policy, because equity distribution allows managers to shift some of their firms’ risk to shareholders. This area of inquiry addresses categories of executive moral hazard, such as misstatements and nondisclosures that place outside stakeholders at a disadvantage; extraordinary efforts to remain in power by fighting takeover attempts that might benefit shareholders; and pursuit of personal objectives (e.g., compensation) through growth ventures or diversification, misusing free cash flow.

ADVERSE SELECTION

Occurs before a transaction or contract because of incomplete information. Incentivizes negative outcomes.

Similarly grounded in the uncertainty triggered by incomplete information, adverse selection refers to situations in which the parties in a contract do not have the same amount of information and one of them exploits exclusive or more comprehensive information.

In the case of insurance, a form of adverse selection is the tendency of less healthy individuals to be interested in more comprehensive health insurance coverage, given that they have more knowledge about themselves and how they use insurance than insurance providers have. To reduce exposure to insurance claims, underwriters evaluate risks before giving an insurance policy that outlines premiums, deductibles and copayments.

Both moral hazard and adverse selection address situations in which one party is at an advantage and exploit that advantage for their own benefit, under conditions of incomplete information or information asymmetry.

The main difference between them is the time of occurrence: in adverse selection, there is a lack of symmetric information before the contract is made or prior to the time when the transaction is agreed upon, while in moral hazard, one party changes behavior after the contract is made or the transaction occurred. In both cases, one party to the contract would have changed the terms of the contract or not offered it at all if they had had complete information.

RISK MITIGATION

Adverse selection and moral hazard are more common when moral standards are low. Examples of low moral standards are the lack of accountability, responsibility and self-centered behaviors. When one party possesses more relevant information than the other party in a contract agreement and sees incentive to engage in riskier behavior than otherwise, that party can take risks, knowing that the others, who are less informed, will share those risks.

Soft measures, such as trust building, establishing code of ethics and moral engagement, as well as hard measures, such as specific contracts and targeted regulation, can mitigate risks. For example, designing self-selection contracts (health insurance) or including warranties, to separate good-quality products from poor-quality ones, since producers, but not buyers, know their quality.

THE MARKET FOR LEMONS

In a widely cited economics paper, “The Market for ‘Lemons’: Quality Uncertainty and the Market Mechanism” George Akerlof refers to an adverse selection problem where high-quality actors (“good apples”) are negatively affected by low-quality actors (“bad apples”), leading to mistrust, distrust and market dysfunction.

The quality of goods in amarket can degrade in the presence of information asymmetry between buyers and sellers, which ultimately leaves only poor-quality goods, even goods found to be defective post-purchase, referred to as “lemons.” Information asymmetry within the market relates to the seller having more information about the quality of the product than the buyer, creating adverse selection, where sellers are not willing to sell high-quality goods at the lower prices buyers are willing to pay, with the result that buyers get lower-quality goods. As enough sellers of high-quality goods leave the market, the average willingness to pay for buyers will decrease because the average quality of goods on the market decreased, leading to even more sellers of high-quality products leaving the market.

Thus, the uninformed buyer’s price creates an adverse selection problem that drives the high-quality goods from the market. This can lead to a market collapse due to lower equilibrium price and quantity of goods traded in the market than a market with perfect information.

MARKET CONTROLS

Alternatively, risks can be mitigated through regulation and control. In the corporate control literature, several forces can operate simultaneously to mitigate moral hazard and promote effective governance: (1) legal and regulatory system; (2) external control mechanisms, such as capital markets, product and factor markets and internal and external labor markets; and (3) internal control and governance (e.g., fiduciary duty, board of directors).

Participants in many markets can use public measures, such as insurance appraisal, universities’ rankings and analysts’ estimates to mitigate adverse selection and moral hazard risks.

Consistent with the agency theory, Jensen and Meckling (1976) support the idea of aligning managers’ interests with those of shareholders through stock-based payment methods or outcome-based incentive contracts that shift risk from shareholders to managers. These risks can also be mitigated through underwriting and contract provisions.

For example, most health insurance contracts judiciously consider optional services or if there could be unforeseeable influence, in nature (i.e., it is a cost-benefit process on the insurance design process weighing marketability with policy price). Specifically, cosmetic surgery may not be covered because it is considered outside of the intent of health insurance or, even specifically, excluded.

THE FINE PRINT

Mitigating moral hazard and adverse selection can explain the complexity of insurance contracts, which can be burdensome from the customers’ perspective, and often part of long contracts, written in small-sized letters, with the objective of removing liability for unforeseeable and undesirable developments.

Small-letter contract provisions can have big implications. They are there to reduce uncertainty and mitigate the risk of moral hazard and adverse selection. Still, there is hope. Insurance companies genuinely desire to offer their clients benefit plans that are useful and cost effective, while also using contractual and legal requirements to protect participants from those who unduly try to take advantage of the system.