From the Professor: Appraisals, Property Taxes and Inflation

By Paul Byrne

Professor of Economics

Brenneman School of Business, Washburn University

Property taxes took center stage this past legislative session as politicians across the political spectrum proposed ways to soften their impact on household finances. The fact that property taxes are determined much differently than income and sales taxes can lead to some confusion for taxpayers.

So how are property taxes determined, and why have they been increasing so much in recent years?

Income taxes and sales taxes are set in similar ways. The government sets the rate and how much a person pays is determined by how much income they earn or how much taxable purchases they make. Most property taxes are determined differently. The first piece of the puzzle is the county appraiser offices, which are responsible for appraising the fair market value of all property within their county.

A property’s assessed value is a function of the appraised value. Commercial and industrial properties are assessed at 25% of the appraised value, and residential properties are assessed at 11.5% of the appraised value.

Some property is exempt from property taxation and is not part of the property tax base. For example, property used exclusively for government, educational, religious and charitable purposes is among the classes exempt from taxation. Governments can also offer property tax exemptions as part of economic development incentives.

County clerks use the appraisals and corresponding assessments to calculate the tax base for each of the jurisdictions authorized to levy property taxes (for example, counties, municipalities, and school districts). Economists refer to these local government entities as overlapping jurisdictions, because taxing jurisdictions have overlapping boundaries. Each jurisdiction has its own property tax base calculated as all of the assessed value within its boundaries.

The next step is that each taxing jurisdiction passes its budget. This is what determines how much property tax revenue will be collected. The tax rate, or mill levy, for each jurisdiction is simply set by the county clerk at the rate at which enough property tax revenue will be raised to meet the budget, given its respective tax base.

People often assume that higher appraisals result in paying more property taxes, but this is not the case. Each property owner is responsible for paying the share of the various governments’ budgets in proportion to their share of the tax base. If your property accounts for 0.001% of the assessed value in your school district, you will be responsible for paying 0.001% of the school district’s property tax collections.

If all property values increase by 10% instead of 5%, your property tax bill will be the same. The mill levy is simply adjusted down as the larger tax base requires a lower rate to cover the budget.

What can cause an individual’s property tax bill to go up? Two things: local governments pass budgets that require more revenue to be collected, or your property’s share of the tax base has increased.

BUDGETS AND INFLATION

When the budgets of the taxing jurisdictions increase, the amount of taxes collected must increase to match the budget. Elected officials will often say “We kept the mill levy the same as last year.” People reasonably take this to mean that their property tax bill will be the same as last year, but it does not. What it really means is that the jurisdiction’s budget grew at the same rate as its tax base, so the property tax bills will increase by the same rate.

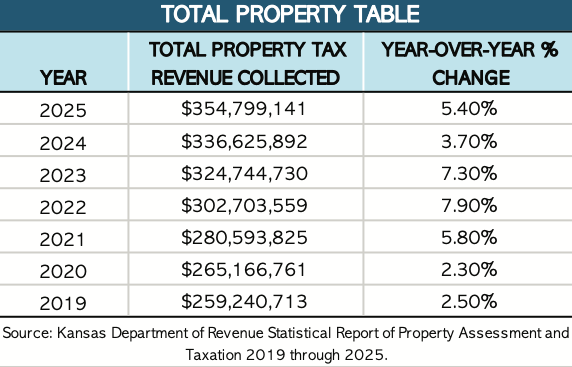

The Total Property table shows the annual percentage change in property tax collections for all Shawnee County jurisdictions (including the state portion) from 2019 to 2025.

2021 through 2023 represented a period of relatively significant growth in property tax revenues. Total tax revenues grew by 7.9% and 7.3% in 2022 and 2023, respectively. One cause of growing budgets can come from governments providing more services: building a new school, adding a mental health unit in the county jail, or expanded road and infrastructure projects.

Another underappreciated source is inflation. The federal government’s large fiscal stimulus during and after the pandemic resulted in more dollars chasing scarce goods. This not only drove up prices for households, it also increased prices for governments.

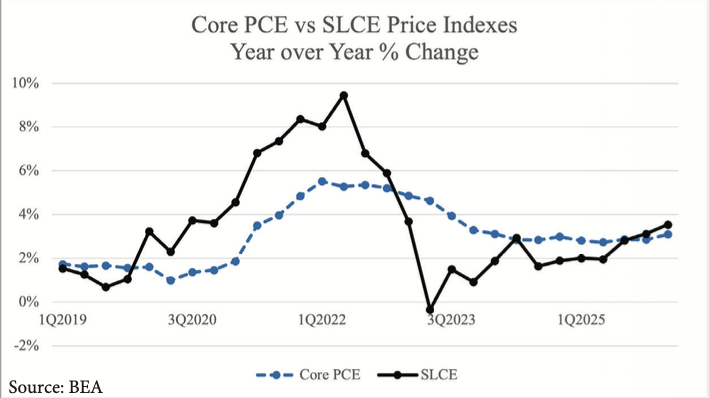

Whereas the Consumer Price Index, or CPI, and Personal Consumption Expenditure Index, or PCE, are regularly discussed measures of household inflation, the Bureau of Economic Analysis’s State and Local Consumption Expenditures Index, or SLCE, measures prices that state and local governments pay for inputs. The following graph compares the quarterly year-over-year change in the PCE versus the SLCE.

While the household inflation measure increased from just under 2% in 2021 to over 5.5% in 2022, state and local governments faced even greater inflation, which peaked at 9.5% in the second quarter of 2022. Most of this inflation was driven by the price of intermediate goods and services, in particular, for non-durable goods.

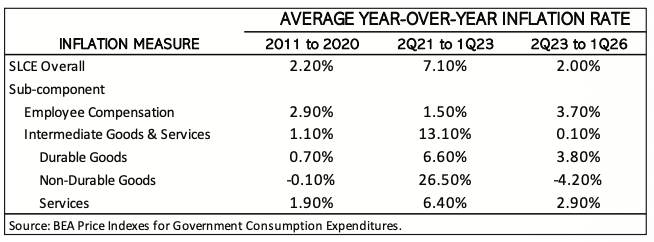

From 2011 to 2020, the overall inflation rate for state and local governments averaged 2.2%, with the employee compensation component experiencing the highest price increases at 2.9%. In the high inflation period from 2021 to 2023, employee compensation inflation was relatively tame at 1.5%. Inflation of intermediate goods and services was 13.1%, driven by 26.5% inflation in the prices of non-durable goods. Since early 2023, state and local government inflation has returned to a more modest 2.0% overall.

Like businesses that face pressure to pass on higher costs of production to consumers via higher prices, inflation in the prices governments pay put pressure on governments to raise taxes. While Americans had become a little dismissive about the dangers of rampant inflation prior to 2021, the last five years have highlighted why economists have always viewed rampant, unexpected inflation as being so damaging to an economy.

CHANGING TAX BASES

When all property values grow uniformly, the share of the tax burden stays constant. However, Shawnee County has experienced a nationwide trend of residential property value growing at a higher rate than commercial and industrial property values. As a result, residential properties bear a growing share of the tax burden.

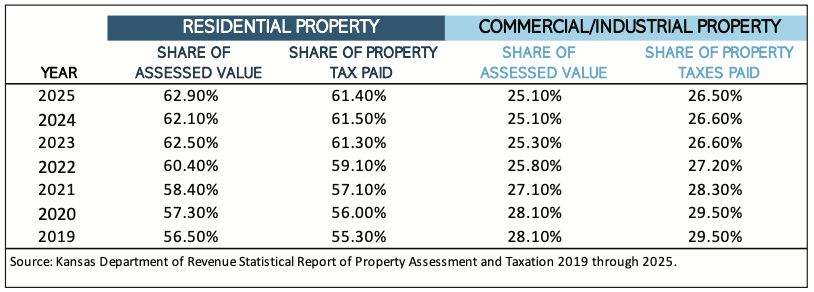

The Residential Property and Commercial/Industrial Property table shows the total share of assessed value and property taxes paid in Shawnee County.

From 2019 to 2025, the total appraised value of residential properties in Shawnee County increased at an annual rate of 7.6%, whereas commercial/industrial properties increased at a 3.7% rate. This has resulted in residential properties’ share of taxes growing from 55.3% to 61.4%.

In 2025, residential properties paid $218 million of the $355 million of property taxes in the county. If residential properties had not experienced higher property value growth rates than other classes and their share of the tax base held at 2019 levels, residential properties would have paid only $196 million of the $355 million of property taxes in the county.

ASSESSMENT GROWTH CAP

In past legislative sessions, some legislators proposed capping a property’s assessed value growth at 3% a year. This would have no impact on the total property taxes paid, which is determined by passed budgets. The cap would require higher mill levies to offset the smaller tax bases.

This results in the tax burden shifting from high-growth properties to low-growth properties, which could be across classes or across neighborhoods. Homeowners in high-appreciation neighborhoods will see taxes decrease while homeowners in low-appreciation neighborhoods will see their property taxes increase.

Compared to the current system where properties are a function of appraised value, assessment growth caps can cause other unintended consequences. For example, newer homes and commercial buildings would pay higher taxes, offsetting dollar for dollar, the decreased taxes paid by older buildings with identical market values.

BALANCING TRADEOFFS

Although not everyone likes comparing governments to businesses, governments and businesses have more in common than many people realize. Taxes are the price residents pay for government services.

Just as customers value both low prices and high quality, taxpayers value both lower taxes and government services. Businesses that fail to strike the right balance risk losing customers; governments that do the same risk losing residents and businesses.

Successful governments, like successful businesses, provide services that people value more than the prices they pay. High inflation makes those tradeoffs harder to navigate for both.