Planning with the end in mind

Consider the following all-too-common scenario:

Jack and Jill own and operate their family business here in Topeka. They have three adult children: Tom, Dick and Sally. Tom stayed in Topeka and worked in the family business all of his life; however, Dick lives in Boston and Sally lives in Los Angeles. Neither Dick nor Sally has an interest in the business. Jack and Jill want the business to continue with Tom in charge but want to treat all of their children fairly when they are both gone. Their life’s work—and wealth—is in the business. How can they treat their children fairly, while also keeping the business going and avoid conflict between their children?

If Jack and Jill failed to make a business succession plan, Tom, Dick and Sally would each inherit a third of the business. Dick and Sally may want cash, and may force their brother, Tom, to accept a fire sale price for his share of the business. Consequently, the business would be gone, and the siblings may never speak to each other again.

Planning

Closely held businesses and family farms involve a number of unique characteristics and considerations. A successful succession requires many issues to be considered, including:

who will be the successor(s),

how, when, and in what manner will such individuals or employees become owners,

how to protect or compensate passive family members.

Practical problems are frequently faced in the business succession context. Contentious disagreements can arise not only between active family members regarding business decisions, but even more so among active and passive family members. These disagreements can be fueled by a perception of an unfair distribution of the parents’ estate or inequitable lack of control.

Unfortunately, many of these important business succession considerations are often either ignored or not addressed in a timely manner. The failure of the family business succession plan raises the ominous specter of significant costs, loss of business value, the potential forced sale of business assets and irreparable family discord.

Planning2

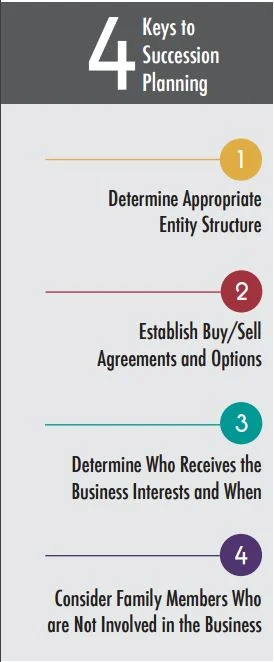

1. Determine Appropriate Entity Structure

Business creation and structure are important to business succession. For those buying a business or property, the exit strategy should be considered before even entering into the deal.

Business interests can be owned by a wide variety of entities, including limited liability companies, limited liability partnerships, family limited partnerships, simple partnerships and corporations. Operating under an entity achieves centralized management, asset protection and continuity of the business.

Entity ownership facilitates management by multiple owners and prevents a minority member from forcing a liquidation of the business. Entity ownership is particularly important with respect to multiple owners in land or other real estate, as any co-owner could unilaterally force a partition, which normally results in a public sale of the land.

Entity ownership can be structured so as to provide non-voting and voting interests, thus permitting active family members to have the voting interests and senior family members to give non-voting interests (normally at substantial discounts in their value for gift and estate tax purposes) to junior family members without losing voting control of the business enterprise

2. Establish Buy/Sell Agreements and Options

A buy/sell agreement is normally the cornerstone of any successful business continuation plan. Such agreements can prevent business interests from being gifted or sold outside the family unit without the active family members being first given the option of purchasing the interests. Under the provisions of the buy/sell agreement, the purchase price of such option held by other active family members can be at the same price offered by the third party (a “right of first refusal”), a price determined annually by family member owners, under a predetermined financial formula, or by appraisal.

A well-drafted buy/sell agreement can:

Prevent involuntary transfers by owners to third parties (e.g., pursuant to a divorce decree or bankruptcy sale).

Provide liquidity at the death of an owner of the business by requiring a mandatory buyout by other members or the entity (often funded with life insurance). Otherwise, the family of the deceased owner of a minority interest could be left with an illiquid, unmarketable business interest, or the remaining owners may now have an unwanted—and often disgruntled—new member in the business.

Prevent what is known as a “freeze out.”Let’s assume Tom, Dick and Sally are all actively involved in the business. Jack and Jill leave the business to the children in equal shares. Following a disagreement over management decisions, Tom and Dick decide to exercise their combined majority control of the stock and “fire” Sally. Sally could be left with no significant employment opportunities and unmarketable stock in a family business that pays no dividends. In such circumstance, under provisions of the buy/sell agreement, the “fired” family member, Sally, could be given a “put option” (the right to force the business or remaining owners to purchase the stock). Without a “put,” Sally could be forced to sell the stock to her brothers for a fraction of its actual value related to its percentage of the total value of the business enterprise.A “put” may discourage maneuverings of family members against another family member in fear that such family member might then decide to exercise the “put” right.

Planning4

Include provisions for “tag-along” and “drag-along” rights. Tag-along provisions help prevent active owners from unfairly benefiting on a sale of the company to the detriment of the passive owners.Drag-along provisions keep the non-voting members from blocking a sale to a third party if the voting member is selling all of his units, and the price meets a minimum amount set forth in the LLC’s operating agreement. Assume Tom has received an offer to purchase the business, but the buyer demands Dick and Sally’s interests as well. Assuming the offering price is in excess of the pre-established price in the operating agreement, Tom can force Dick and Sally to sell as well.

3. Determine Who Receives the Business Interest and When

Family members are the likely candidates to continue the business, but, if no family members are interested in taking over the business or possess the necessary skills to competently manage it, the most likely business successors may be key personnel or management.

If none of Jack and Jill’s children were involved in the business, they could grant a key employee options to purchase the business interests during life or out of their estate. The options may include a payment schedule, secured by the business interests. In this case, Tom, Dick and Sally would be paid for the value of the business, but it would be paid from a third person over a period of time. Their inheritance would consist partly of a note from the new owner.

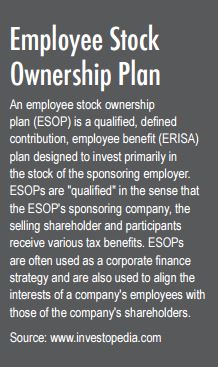

Another option would be for Jack and Jill to create an Employee Stock Ownership Plan. The ESOP could take out a loan and purchase Jack and Jill’s interests. The loan could be paid off over time from the business income. Jack and Jill would have liquid assets to divide among their children, and their employees could be in control of the business through the ESOP.

If the decision is made to not continue the business, liquidating or selling the business obtains the maximum economic value. For such businesses, it is especially important that key employees remain operative in the business following the owner’s death to maintain economic viability until the business can be sold. Entering employment contracts containing non-compete covenants can also be crucial in order to prevent employees from taking the good will, customer lists, and any trade secrets of the business during and following their employment.

4. Consider Family Members Who Are Not Involved in the Business

One of the biggest problem areas in transferring business interests is the treatment to the accorded family members who are not involved in the business. When both active and passive family members inherit a closely held business, there frequently will be disagreements. Often, passive family members may disagree with the active member’s management, feel that such active family members prefer themselves in terms of salaries, conclude that distributions of business income to them is not commensurate with their ownership interests, or simply resent not having received liquid assets.

On the other hand, providing a greater share of the estate solely for the purpose of ensuring that only active family business members will receive the business interests can trigger disagreements and feelings of resentment from passive family members who receive less. This is also often inconsistent with the parent’s desire for fair treatment of all children from an inheritance standpoint.

Strategies for addressing this situation vary considerably. Business interests can be given to all family members, restricting management decisions to active family members, while at the same time structuring the business enterprise so as to equitably address the financial interests of passive family members. Under this scenario, passive family members are usually given non-voting interests in the business. Such interests can be given preferential distribution rights (e.g., preferred stock) to balance against the active family members controlling both the business and distributions of salaries and business income.

Jack and Jill addressed these issues in their succession plan. Their LLC includes voting and non-voting interests, which are still entitled to equal distributions of business income. Tom will receive voting interests, and Dick and Sally will receive non-voting interests. But their total interests will grant equal rights to income and Dick and Sally’s interests will have a preference on liquidation.

The LLC also includes buy/sell provisions, which require any owner who wants to sell to first offer their interest to the LLC and other owners. The non-voting interests have “put” rights, which allow the non-voting owners to force the LLC and voting owners to purchase the non-voting interests at an agreed price but payable over a 10-year term with minimal interest. But the “put” right cannot be exercised until five years after Jack and Jill’s death. Thus, Dick and Sally could force Tom to buy their interests, but they could not exercise this right until at least five years after Jack and Jill died, and Tom could buy them out over 10 years.

Conversely, Tom’s voting interests have “options” to purchase Dick and Sally’s interests at a specific price, which is higher than the “put” price and must be paid in a cash lump sum. If Tom wants to buy out Dick and Sally, he has to pay cash and pay a premium. Lastly, the LLC includes “tag-along” and “drag-along” rights to keep Tom from unfairly benefiting on a sale of the company and Dick and Sally from unfairly blocking a sale that may be in the best interests of all involved.

As you can see by this example, it is critical that business owners who desire to effectively continue the business consult experts in succession planning to create and implement a business succession plan.